This report, to which I contributed, has been published and can be read without needing to download, on the Steady State Manchester website here. In a nutshell, it provides a vision (and practical ideas) for building an alternative future economy that is more sustainable than the one we currently operate. The main thrust is to challenge the notion that perpetual economic growth is both possible and desirable. The main constructive suggestion is to re-envision a future economy where growth (in aggregate) is neither desirable nor necessary in order to achieve a fair, balanced and sustainable future for subsequent generations.

|

This recent news item about the forthcoming Energy Bill is disappointing regarding carbon targets for the UK. However, the silver lining is that at least the Government is increasing the amount of subsidisation of low carbon energy.

I've rehoused our latest batch of seven half-grown chickens in larger accommodation, as they've outgrown the guinnea pig cage they were in. The two chicken arks (one of which is pictured) were ones I designed and made myself a couple of years ago.

The half-grown cat gives an idea of the scale. I’ve been referring back to my dog-eared copy of “Positive Economics” by Richard Lipsey. This book, published in 1963, is nearly as old as I am. It was written before mainstream acceptance of sustainability challenges (eg climate change). It also pre-dated the seminal works on ‘limits to growth’, which were in the mid-seventies. However, even despite this, it outlines very clearly some of the most important features of money and what it means to us, and in a way that has clear messages for us in terms of what money was once, and what it could be again – a store of value directly connected to assets that we value and want to preserve and expand.

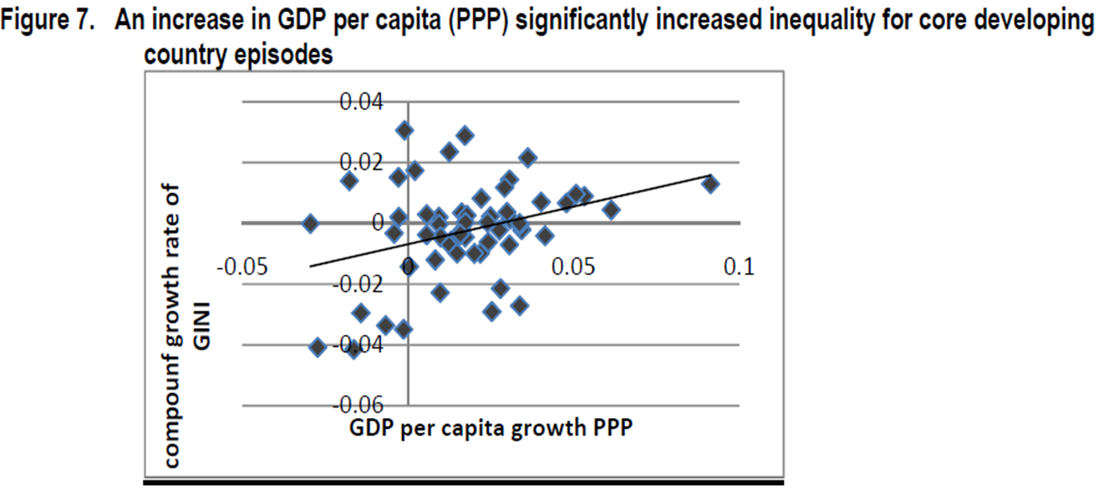

There’s a particularly good section on the implications of most currencies around the world having left the gold standard in the years between the First and Second World Wars. It includes the following quote: “In general, a gold standard is probably better than having the currency managed by an ignorant or irresponsible government ...” Lipsey also talks about some of the historical advantages of having such an asset-backed currency, including: “Tying a currency to gold meant ... it provided a check on the prince’s ability to cause inflation. Gold cannot be manufactured at will; paper currency can ... the gold standard provided some check on inflation by making it difficult for governments to change the money supply. ” Lipsey notes some of the downsides of asset-backed currency, including inflation when there were major gold discoveries. Replacing the role of gold in an asset-backed currency with a unit of sustainably managed land (without using a fractionally backed approach), however, would make this problem far less significant. Indeed, it would generate an incentive for beneficial actions, because the creation (or conversion) of (privately owned) land to sustainably managed land would actually be a good thing while at the same time being wealth-creating for the landowner. Of necessity, governments or central banks would need to own (or control) significant reserves of sustainably managed land in order to provide this asset backing to their currencies. Not a problem, though – they already own much land and could always use compulsory purchase powers to create adequate levels of such reserves within a balanced economy and ecosystem. This new form of currency, which one could call, for example, the Ecopound, providing it was taken up by reputable governments and central banks, could provide all the benefits of being a medium of exchange, but could also provide a store of value (overcoming some of the shortcomings of gold in this respect) while encouraging the maintenance (and expansion) of the stock of sustainable land which backs it. By the very nature of the finite supply of the asset backing, this currency would protect against the worst boom-and-bust cycles of existing economic cycles, by providing a stable and limited supply of the asset (and therefore of the money supply). It would also prevent a recurrence of the financial meltdown of circa 2008 and the fall of banks such as happened to Northern Rock at that time. The main parties to lose out under this scenario would be the banks, especially because of the move away from fractional backing. As Lipsey points out: “... each bank was able to issue more money redeemable in gold than it actually had gold in its vaults. This was a profitable thing to do, because the bank could invest its newly created money in interest-earning assets.” Perhaps this would also provide a further driver for the existing trend of the separation of investment banks from retail (transactional) banks. The former depend on investing for a return, the latter exist to support the use of money as a medium of exchange and store of value for ordinary, individual citizens. Under the asset-backed Ecopound concept, there might not be as much business for the investment banks, but there would still be plenty of business for the retail banks. The main perceived ‘downside’ might be the constraints this would put in place on economic activity (perhaps limiting money available for lending and growth). However, this might actually be an advantage, especially for anyone supporting a transition to a steady-state economy.  I'm trying out some of the newest low-energy LED light bulbs available in the mainstream market. I'm replacing some earlier-generation bulbs (1 or 2 Watts) with new ones, because my wife is complaining that the existing ones don't throw enough light. The picture on the left shows one of the new bulbs, in GU10 fitting - I've bought some 4W bulbs and some 5W. Both the 4W and 5W units look very similar to each other. The strategically placed cat's paws give a sense of the scale. The picture below shows the new bulbs in action (again, with the cat getting involved to help dress the scene). The old bulbs are now in other parts of the house, replacing older 50W bulbs.  The UK is officially out of a four-year recession, because the economy grew by a fraction of a percent last quarter. Although many people will sigh with relief (especially politicians in power), the percentages are so small that little can be concluded about the longer-term trends. For all we know, this could be a temporary upswing on a flat long-term trend. These politicians would love this to be the sign that we’re ‘heading back to growth’. They see it as largely their role and their mantra to achieve economic growth. Their belief (or at least their hope and the reason they think they’ll be re-elected) is that growth = new jobs and other tangible signs of prosperity. In turn, this prosperity is meant to solve poverty. Unfortunately, some evidence suggests that, despite growing prosperity in many countries, the poor and vulnerable sections of society still remain poor and vulnerable. For an example of evidence about this, see "What has really happened to poverty and inequality during the growth process in developing countries?", a paper from the ILO. The following diagram is from the report.  Growth without other measures does not solve these problems. Indeed, in some ways it exacerbates them because it makes the gaps between the richest and the poorest more visible and therefore socially painful. It’s a shame that this doesn’t spur politicians to take stronger action on social justice once they’re in power, rather than just assuming that growth will solve it. Perhaps, counter-intuitively then, politicians should instead work to restrict growth, work towards a‘steady-state economy’ or for actual shrinkage of the economy. This way, the gap between the richest and poorest would become smaller and social justice wouldn’t appear to be such a problem, assuming the social welfare safety net for the poorest and most vulnerable could be successfully maintained at suitable levels despite such economic conditions. It’s worth reflecting for a few moments on the consequences of our historical love affair with economic growth and why we might have become so attached to it over the centuries. In a conversation about money, credit and the economy recently, an Alderman of the City of London recently asked me what our lives would have been like today if we had not had decades (centuries, in fact) of growth fuelled by the concepts and practices of modern banking. “Well,”I said, “our standard of living would not be as high as it is today, but then again we wouldn’t be facing as severe a challenge to live within the planet’s limits to support us, and might not therefore be facing catastrophic climate change, among other sustainability issues. Our task to address these issues would not be as great, our legacy to our children and grandchildren not as frightening”. There’s a practical consideration here, in that we would miss our current wealth if we had it taken away now. However, would we have “missed” our ability to achieve our current standard of living if we had never grown fast enough to achieve it? Can you ever miss something you never had (or never knew could exist) in the first place? It is debatable whether we can (or have a right to) feel aggrieved to miss out on future increases in standard of living (through future growth) if we forego that growth from now on (assuming we have any choice in the matter). However, it is becoming increasingly clear that resource (and ecosystem) constraints are affecting us in many ways (including climate change) and these effects can only get stronger as the global population grows (even if it peaks at 9 or 10 billion compared with the 7 billion alive today). On the other hand, we shouldn’t assume that the recent recession is strong evidence of the effects of ‘limits to growth’ kicking in at a planetary level. It would take a decade or two of solid trend data to convince most people that these limits were kicking in at a whole-economy and global level. Having said that, I wouldn’t know what the statistical analysis would tell us is the number of years of continuous recession that would have to occur before we could say, with statistical certainty, that these limits were being reached and a permanent shift had occurred in the underlying drivers of the economies around the world. Economists and mathematicians might at this point talk about ‘relevant ranges’, ie ranges of operating conditions, measurements etc within which the rules, within which we might have to date assumed we have been operating, are ‘valid’ (ie an accurate way of describing the real world and predicting the future). Outside these ranges of conditions, however, new rules and calculations govern our world (and our economies). In fact, these ‘new rules’ were always there in the economists’ calculations – it’s just that their size and impact on the end results were so small that they made no difference‘within the relevant range’. Once outside the relevant range, those numbers become big enough to become key drivers of the end results. So, have we stepped outside these relevant ranges yet? This is the key question, for me. It leads on to questions about reversibility. If you’re outside a relevant range, can you get back inside it, or are there connected effects and consequences that drive your position further and further outside, and possibly accelerate them towards new operating ranges or equilibria? This gets into the realms of talking about ‘tipping points’, being those points where the system is tipped from one range or equilibrium into another one (which might possibly be more hostile to human existence). Hence, if there is such a ‘tipping’, and if one can predict it in advance, isn’t it also sensible to examine whether there is reversibility, ie an ability to act to reverse previous trends and ‘tip back’ to the previous range and equilibria? If there is reversibility (with confidence) , then it would reduce the pressure to avoid the tipping point. It would seem sensible to avoid a knee-jerk reaction to the tipping point in some circumstances, for example if this could only be done with excessive haste and inefficient redirection of massive resources. Perhaps this line of reasoning might increase the argument for research, analysis and planning for the tip-back under those circumstances. In fact, irrespective of the above argument, it seems a no-brainer to increase reversibility wherever possible in ecosystem elements or components, as this increases the likelihood of tipping-back the whole system (or preventing its tipping-over in the first place). A simple and practical example of this is reversibility conditions placed on development of land, such as in the Lammas development in Wales. The greater the number of reversible situations we can put in place, the greater the number of levers we have that can be pulled to prevent a tipping point being reached or to tip us back after one has been reached. So perhaps a slightly easier concept to sell than “sustainability” might be “reversibility”. |

About the BloggerI'm David Calver - an Accountant with a passion for sustainability. Categories

All

Archives

February 2016

|

RSS Feed

RSS Feed